Artificial intelligence is fundamentally challenging the long-standing correlation between employee numbers and business output. Block has cut roughly 40 per cent of its workforce. JPMorgan is redeploying nearly 320,000 employees internally. AI-native start-ups with as few as ten people are generating revenues once reserved for much larger organisations. What they all share: AI is reshaping the equation that has long tied headcount to value creation.

Artificial intelligence is changing the traditional equation, in which greater output requires proportionally more staff.

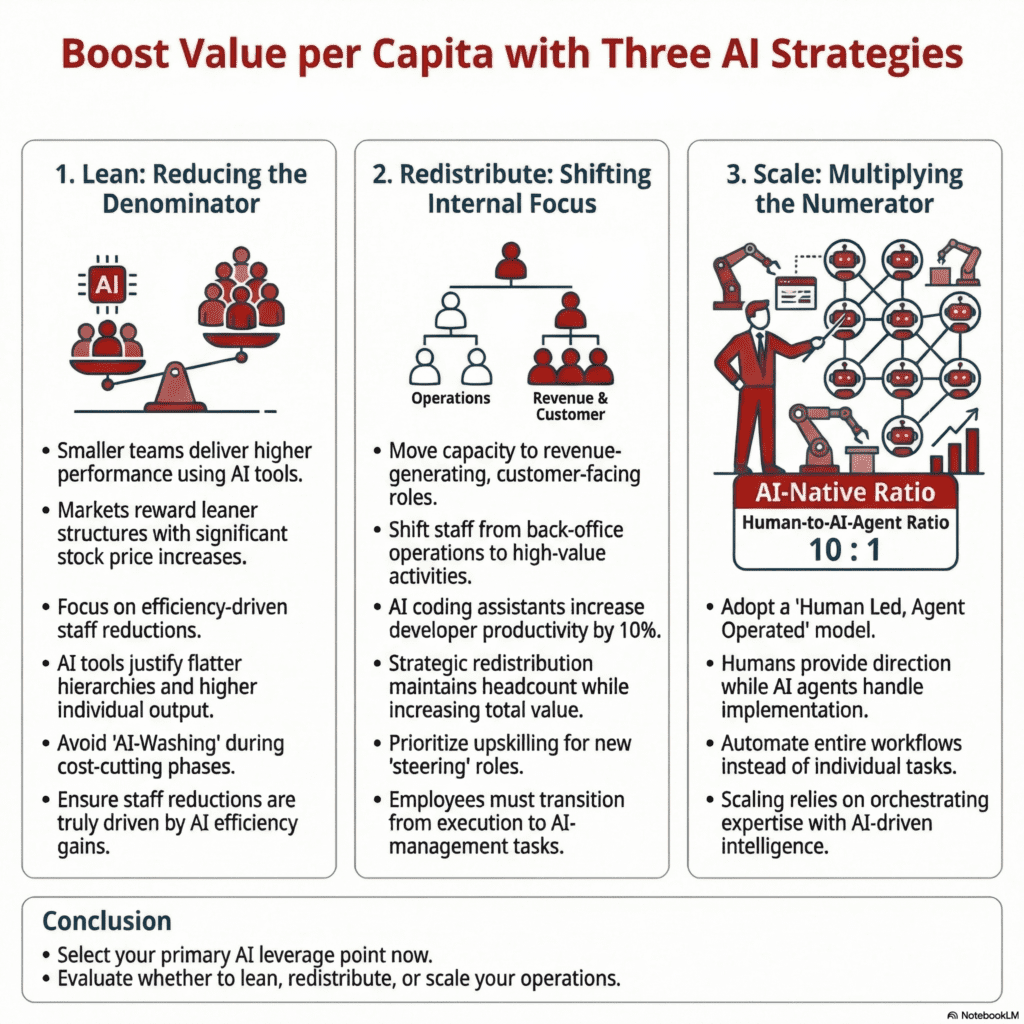

- Block has cut 40 per cent of its workforce, citing AI-driven efficiency (Strategy 1: Streamline).

- JPMorgan Chase is keeping the headcount stable whilst shifting roles from operations to revenue-generating functions (Strategy 2: Redeploy).

- AI-native start-ups are achieving the output of much larger organisations with fewer than ten employees and hundreds of AI agents (Strategy 3: Scale).

Is AI upending the traditional equation between workforce size and business output?

In late February 2026, Jack Dorsey, founder and CEO of payments company Block, published an unusual announcement on X. The company would reduce its workforce from over 10,000 to under 6,000 — not because the business was struggling, but because AI-powered tools were enabling a fundamentally different way of working [2]. Days earlier, Jamie Dimon, CEO of JPMorgan Chase, had outlined a different approach: no AI-driven redundancies, but an AI-driven redeployment of roles across the bank’s nearly 320,000-strong organisation — as tasks in operational areas are increasingly handled by AI, whilst new, higher-value positions emerge for existing employees to fill [5]. And at the World Economic Forum in Davos, founders of AI-native companies described how they operate with fewer than ten employees yet hundreds of AI agents, achieving an operational capacity that was previously the preserve of much larger organisations [3].

Three examples, three strategies, but one common thread: artificial intelligence is changing the relationship between workforce size and value creation. The traditional equation, in which more revenue requires proportionally more employees, is losing its validity.

What does this shifting equation mean for SMEs — the organisations operating between the extremes of large corporations and AI-native start-ups? One thing is clear: AI will transform every organisation. The strategic question is therefore not whether this will happen, but which path a company chooses to take.

Why does AI have such a profound impact on these traditional patterns?

The idea that productivity can rise without a corresponding increase in employment is not new. Economist Erik Brynjolfsson identified this paradox over a decade ago [4]. Technology companies such as Apple, Microsoft and Google require significantly fewer additional employees for each successive $100 billion revenue milestone — a pattern also visible in non-tech companies such as Walmart [4].

The critical difference: these efficiency gains primarily concerned scaling existing business models through automation and digitalisation. What AI changes fundamentally is illustrated by the third example from Davos: a start-up with fewer than ten employees and hundreds of AI agents, generating value that would previously have required a much larger workforce [3]. This is genuinely without precedent. AI does not merely automate processes — for the first time, it takes on knowledge-intensive, creative and managerial tasks that were previously the exclusive domain of human expertise. This shifts not only the pace of the decoupling, but its very nature.

Value creation per employee — what are the three core strategies?

Three fundamental strategies are emerging through which organisations use AI to actively reshape the equation between headcount and value creation.

Strategy 1: Streamline — How AI is justifying workforce reductions

Block’s decision is among the most visible cases of an AI-justified workforce reduction at a publicly listed company, generating considerable attention and wide-ranging commentary. Jack Dorsey justified the move as a fundamental shift in how work is done: smaller teams with flatter hierarchies can achieve more with AI tools. He further predicted that the majority of companies would reach similar conclusions within a year [2].

The market response was unambiguous: Block’s share price rose by more than 24 per cent following the announcement [8]. A signal that other boards can scarcely ignore.

The debate surrounding this move, however, deserves nuanced consideration. Analysts point out that Block had expanded its workforce from roughly 3,900 to over 12,000 between 2019 and 2022 — a growth phase driven by pandemic-era demand [8].

Block is not alone. Pinterest, CrowdStrike and Chegg have also recently attributed workforce reductions directly to AI-driven efficiency gains [8]. Regardless of how much AI actually drove these decisions, the dynamic is clear: markets reward leaner structures.

It is worth noting, however, that according to outplacement firm Challenger, Gray & Christmas, only around 55,000 job cuts in the United States during 2025 were explicitly attributed to AI — out of 1.17 million total redundancies. That is less than five per cent [9]. Critics describe this as “AI-washing”: the phenomenon of companies framing conventional cost-cutting measures as AI-driven [6].

Strategy 2: Redeploy — How AI shifts roles without cutting positions

JPMorgan Chase is pursuing a fundamentally different approach. The company continues to employ roughly 320,000 people, but is shifting internal weightings: operational roles declined by approximately four per cent, support functions by two per cent, whilst revenue-generating and client-facing positions grew by four per cent [5]. This approach uses AI not as a tool for headcount reduction, but as a lever for reallocating capacity towards higher-value activities.

The AI-driven efficiency gains at JPMorgan Chase are measurable: according to the bank’s investor presentation, software engineers working with AI coding assistants are roughly ten per cent more productive, operations teams handle six per cent more accounts per employee, and per-unit fraud costs have fallen by eleven per cent through AI-powered detection. Approximately 150,000 of the bank’s employees use its internal AI platform weekly, built on models from OpenAI and Anthropic [5]. JPMorgan Chase’s technology budget stands at nearly $20 billion annually — the largest in the industry [5].

Jamie Dimon, CEO of JPMorgan Chase, has publicly cautioned against pursuing AI implementation in isolation from workforce planning. His argument: certain tasks have already been eliminated by AI, and the affected employees have been transitioned into new roles within the bank. At the same time, he warned of the societal consequences should this transition unfold without adequate planning [5].

The challenges inherent in this approach are considerable. Redeployment demands comprehensive upskilling and reskilling programmes, changes job descriptions and competency profiles, and cannot be implemented with equal success across all employees. The transition from an executing role to an interpreting or directing one requires capabilities that must first be developed — a challenge explored in detail in our article AI First means new skills: why all employees need to understand AI management. According to a 2026 Deloitte study, only 33 per cent of organisations are actively redesigning career paths and internal mobility in response to AI [10].

Strategy 3: Scale — How AI agents multiply output per employee

The third strategy is most visible in AI-native companies but is gaining relevance for established organisations as well. At the World Economic Forum in Davos, Yutong Zhang, President of Moonshot AI, described start-ups with fewer than ten employees deploying hundreds of AI agents for operational tasks — generating value that would previously have required a far larger workforce [3]. The concept is one of high operational leverage, in which AI does not merely automate individual tasks but permeates entire workflows as a collaborative partner.

The World Economic Forum identifies five characteristics of such AI-native operating models: adaptive feedback loops, documented contextual knowledge — an aspect explored further in our article on why tacit operational knowledge is the blind spot of every AI implementation —, clearly defined data standards, early involvement of production teams, and real-time evaluation of outcomes [3]. The approach does not begin with the question “Which tasks can AI take over?” but with the more fundamental question: “If we had access to unlimited intelligence, what would we build?” [3].

This trajectory follows a logic we describe as the AI Evolution: from individual users, through AI-supported teams, to organisations where humans set direction and AI agents handle execution — “human-led, agent-operated”. Human-to-AI ratios in such organisations reportedly already exceed 10:1 — ten AI agents per human employee [3]. What this means in practice and which prerequisites are necessary is something we explore in AI agent teams: the next evolution in enterprise AI. What determines performance is no longer headcount, but the ability to orchestrate human expertise with AI-powered intelligence.

Can the three AI strategies be clearly separated — or do they overlap?

In practice, the three strategies can rarely be cleanly distinguished. Even Block, which took the most radical step, is also redistributing tasks internally and expecting significantly higher output per remaining employee. JPMorgan Chase, meanwhile, is reducing operational roles whilst growing client-facing ones — strictly speaking, more of a redeployment than a streamlining exercise, given that overall headcount remains stable. And AI-native start-ups focused on scaling will inevitably need to shift or redefine roles as they grow, in line with the “human-led, agent-operated” model.

The three strategies therefore describe not mutually exclusive alternatives but possible strategic emphases. The key difference in reshaping the equation lies in the starting point: streamlining addresses the denominator (fewer people), redeployment addresses the deployment (different roles), and scaling addresses the numerator (more output). Most organisations will employ all three levers over time — what matters is which one forms the strategic entry point and delivers the greatest leverage.

What can SMEs take from these strategies?

The cases described originate from the corporate world and from AI-native start-ups. SMEs operate between these two poles — without the resources for billion-dollar redeployment programmes, but equally without the luxury of building AI-natively from scratch. Yet the underlying dynamic affects them in a particular way.

The DIHK Workforce Report 2025/2026 shows that skills shortages are now more pronounced among SMEs than among large corporations. Between 44 and 47 per cent of companies with 20 to 999 employees report difficulties filling vacancies [7]. Eighty-three per cent of all surveyed companies expect the situation to worsen in the coming years [7]. At the same time, according to Bitkom, approximately 109,000 IT positions remain unfilled across the German economy.

Where this trajectory may lead in the longer term is illustrated by East Asia. Japan recorded a record population decline of over 900,000 in 2024, with nearly 30 per cent of its population aged over 65 [11]. South Korea’s working-age population could halve within 40 years, according to Morgan Stanley [12]. Both countries are investing heavily in AI and robotics — not as a strategic option, but as a response to a shrinking labour market that leaves no other alternative. Germany, from a demographic perspective, is on a similar trajectory, albeit with a discernible time lag.

In this context, a realistic development path is emerging for SMEs that combines Strategy 3 and Strategy 1: first, achieve more with the existing workforce through AI support — Strategy 3 as the entry point, a theme we explore further in AI productivity in SMEs: when will the breakthrough actually arrive?. Then, as positions become vacant due to retirement and cannot be filled because of labour market conditions, Strategy 1 gradually takes effect: maintaining or growing output with fewer people. It is important to note: this path is a projection, not a certainty. But the demographic data from the DIHK report and the experiences of Japan and South Korea suggest it could become reality for many SMEs.

However, a significant implementation gap stands in the way. Christina Raab, Managing Director of Accenture Germany, noted at the World Economic Forum in Davos that fewer than half of employees feel prepared for working with AI. Particularly problematic is the lack of communication: only a very small proportion report that their leaders discuss what AI concretely means for their day-to-day work [1]. This silence generates uncertainty and slows the pace of adoption. This is precisely where an approach we call “Leadership First” comes in: equipping the leadership team to understand and model AI strategically before the organisation-wide rollout begins — a principle described in more detail in our article on AI strategy for SMEs.

Raab calls for a paradigm shift: away from “Human in the Loop” — purely supervisory involvement — towards “Human in the Lead”, in which employees actively interpret, evaluate and make decisions based on AI outputs [1]. A principle we examine in depth in AI decisions in business: why humans must remain the final authority. For SMEs, this means that introducing AI tools is the simpler part. The more demanding challenge lies in preparing the organisation — leadership, communication and capability development — for this new way of working.

Streamline, redeploy or scale — which AI path suits your organisation?

The three strategies — Streamline, Redeploy and Scale — do not exist as either/or choices but as parallel levers with varying implementation potential depending on an organisation’s starting position. Block and JPMorgan Chase represent the extremes of a spectrum on which every organisation must find its place.

For SMEs, the combination of Strategy 3 and Strategy 1 is likely the most realistic path in many cases: first, use AI to maintain or ideally increase output per employee, then gradually become leaner as demographic pressures reduce the available labour pool. This also implies that AI need not lead to redundancies but can, on the contrary, strengthen organisational resilience — which in turn safeguards jobs. Yet precisely this path requires leaders who actively shape the AI transition rather than treating it as a purely technical initiative.

AI is increasingly shifting from a cost-reduction instrument to a growth driver and resilience factor [1]. The decisive question is no longer whether AI will transform an organisation. It is how that transformation can be actively shaped and supported.

Sources

[1] Handelsblatt/dpa — “Top consultant: Major perception gap regarding AI in companies”. Christina Raab, Managing Director of Accenture Germany, at the World Economic Forum in Davos. January 2026. https://www.handelsblatt.com/dpa/kuenstliche-intelligenz-top-beraterin-grosse-wahrnehmungsluecke-bei-ki-in-unternehmen/100193483.html

[2] Jack Dorsey — Communication to Block employees and shareholder letter, published on X. February 2026. https://x.com/jack/status/2027129697092731343

[3] World Economic Forum — “How AI-first operating models unlock scalable value”. Maria Basso, Michael Römer. February 2026. https://www.weforum.org/stories/2026/02/how-ai-first-operating-models-unlock-scalable-value/

[4] 36kr — “$4 Trillion with Just 36,000 People: NVIDIA Unveils Harsh Truth — Labor Decoupling from Wealth”. November 2025. https://eu.36kr.com/en/p/3558186189044608

[5] CNBC — “Jamie Dimon says AI is already reshaping JPMorgan Chase’s workforce as bank plans ‘huge redeployment'”. February 2026. https://www.cnbc.com/2026/02/24/jpm-ceo-jamie-dimon-ai-reshaping-workforce-redeployment.html

[6] Bloomberg — “Jack Dorsey’s 4,000 Job Cuts at Block Arouse Suspicions of AI-Washing”. March 2026. https://www.bloomberg.com/news/articles/2026-03-01/jack-dorsey-s-4-000-job-cuts-at-block-arouse-suspicions-of-ai-washing

[7] DIHK — Workforce Report 2025/2026: “Skills shortages remain a challenge”. December 2025. https://www.dihk.de/de/newsroom/fachkraeftereport-2025-2026-engpaesse-bleiben-eine-herausforderung-159846

[8] Fortune — “Block CEO Jack Dorsey lays off nearly half of his staff because of AI and predicts most companies will make similar cuts”. February 2026. https://fortune.com/2026/02/27/block-jack-dorsey-ceo-xyz-stock-square-4000-ai-layoffs/

[9] Built In / Challenger, Gray & Christmas — “Did AI Take Your Job? The Truth About AI Washing”. March 2026. https://builtin.com/articles/ai-washing-layoffs

[10] Deloitte — “The State of AI in the Enterprise 2026: The Untapped Edge”. Survey of 3,235 leaders across 24 countries. January 2026. https://www.deloitte.com/global/en/issues/generative-ai/state-of-ai-in-enterprise.html

[11] Bank of Japan / ISDP — Data on Japan’s demographic development. Population decline 2024, share of population aged 65+. https://www.isdp.eu/the-demographic-deficit-national-security-challenges-for-japan-and-south-korea/

[12] Morgan Stanley — “South Korea Population Decline Crisis”. Projection on working-age population development. https://www.morganstanley.com/ideas/south-korea-population-decline-aging-crisis

Would you like to strategically implement AI in your daily business operations?

The question is: What does this look like in your company? Do your employees have the competencies they need for this new work reality? Or are AI integration and competency development currently happening side by side – without systematic connection?

In a no-obligation strategy session, we would be happy to introduce you to the NordAGI approach.